Fraud, Fund Risk Management Failures and The Alternative Investment Standards

In May 2022, the US SEC announced charges on an investment manager relating to fraud and fund failures in their structured products. The more than $6bn fine is among the largest in corporate history and was accompanied by criminal charges against the former CIO and two other portfolio managers.

The enforcement relates to four actions:

- Manipulating numerous financial reports and other information provided to investors,

- Materially misrepresenting to investors, the levels at which hedging positions were in place,

- The CIO causing the portfolio management team not to implement an agreed risk mitigation program and then hiding this to increase his own compensation, and 4.

- Misrepresenting that the strategy had a capacity limit of $9bn for certain funds and the CIO causing that limit to be exceeded by more than $3bn

Are Derivatives and Complex Products to Blame?

While some have blamed the use of derivatives and product complexity for causing investor harm, we at the SBAI believe that it is ultimately failures in risk management, governance and compliance processes and controls that are the cause of this unexpected loss to investors. Had the positions been hedged correctly or the risk mitigation programme been implemented, perhaps the losses would not have been as large. If investors had been made properly aware of the actual volatility of the product, they could have made informed decisions on whether the level of risk was appropriate for them.

The case raises broader questions about the safeguards that investment managers need to put in place to prevent bad actors from committing fraud and help investors detect weaknesses in such safeguards.

How Can the SBAI Alternative Investment Standards Help?

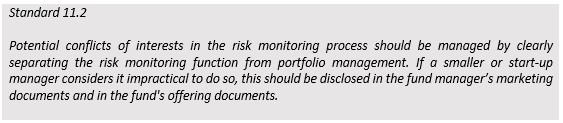

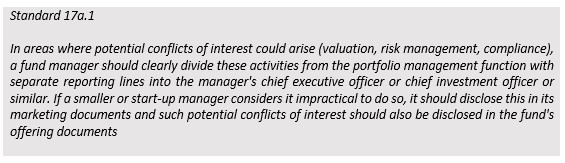

Here we look at some of the key failures in this case and how compliance with the SBAI Alternative Investment Standards could have helped prevent or mitigate some of these failures. Whilst it will not always be possible to stop a determined bad actor, there are controls and processes that can be put in place to make it more difficult for the bad actor to act and easier to spot. Two key standards that would have helped to prevent these failures:

Both standards cover the independence of the risk management function from the portfolio management function. In this case, the CIO was able to falsify risk reports, not place the required hedges and cause a risk mitigation programme not to be put in place. Had there been an independent risk function, these actions would have been made more difficult and perhaps prevented or rectified promptly.

Whilst our Standards make some allowances for small and emerging managers, the firm in question did not fall into this category and would have been able to put in place an independent and segregated risk function.

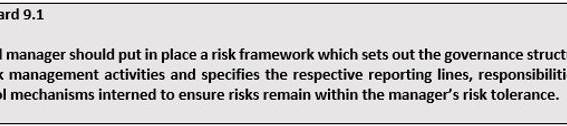

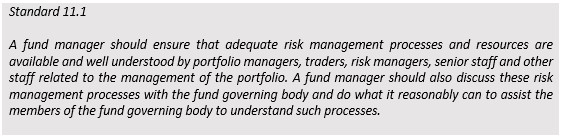

When proper independence of the risk management process is in place, our Standards cover a number of ways in which risk should be governed and reported, including:

In this case, the hedges that were not being placed and the failure to implement the agreed upon risk mitigation process would have resulted in a material change to the fund’s risk profile which should have been disclosed to investors.

Had a risk framework been in place with an independent risk function, it would have detailed portfolio risks both for investors and indirectly for the asset managers and the mechanisms for ensuring that the risk remained in the appropriate risk tolerance threshold.

All staff should have been made aware of the risk management processes which may have helped identify breaches.

What Role Can Independent Fund Boards Play?

At the SBAI, we believe that strong fund governance arrangements, including fund boards with a majority of independent directors, play an important role in mitigating the risk of bad actors. The Alternative Investments Standards set out the collective expertise expected from independent boards and we also set out the key items to be covered in fund board meetings in our Standardised Board Agenda including:

- Investment Management Report: Provided by the fund manager, this report includes a dedicated Fund Risk Report, and confirmation that investments have been made inline with the investment objective and restrictions disclosed in the fund's offering document.

- Operations Report: This report risk oversight, including reviews of risk policies, monitoring procedures and reporting, and reporting of breaches of investment restrictions.

Conclusion

The Alternative Investment Standards and other SBAI Toolbox memos, such as the Standardised Board Agenda, provide a range of safeguards including robust risk management processes and controls, reporting to and oversight by the fund governing body and reporting to investors enabling them to make well informed investment decisions. To mitigate the risk of bad actors, these standards are most effective when combined with an independent risk management function. Compliance with the SBAI Alternative Investment Standards would require this.

Find out more about the Alternative Investment Standards here.